One year after the EU elections, Europe finds itself in a fraught political climate marked by discussions around climate targets, rising tensions with China and the US, and turbulences in global markets. Against this backdrop, it is now more than ever imperative that Europe sets itself apart with bold and strategic solutions to counter these challenges and ensure a strong, sustainable economic future for the continent.

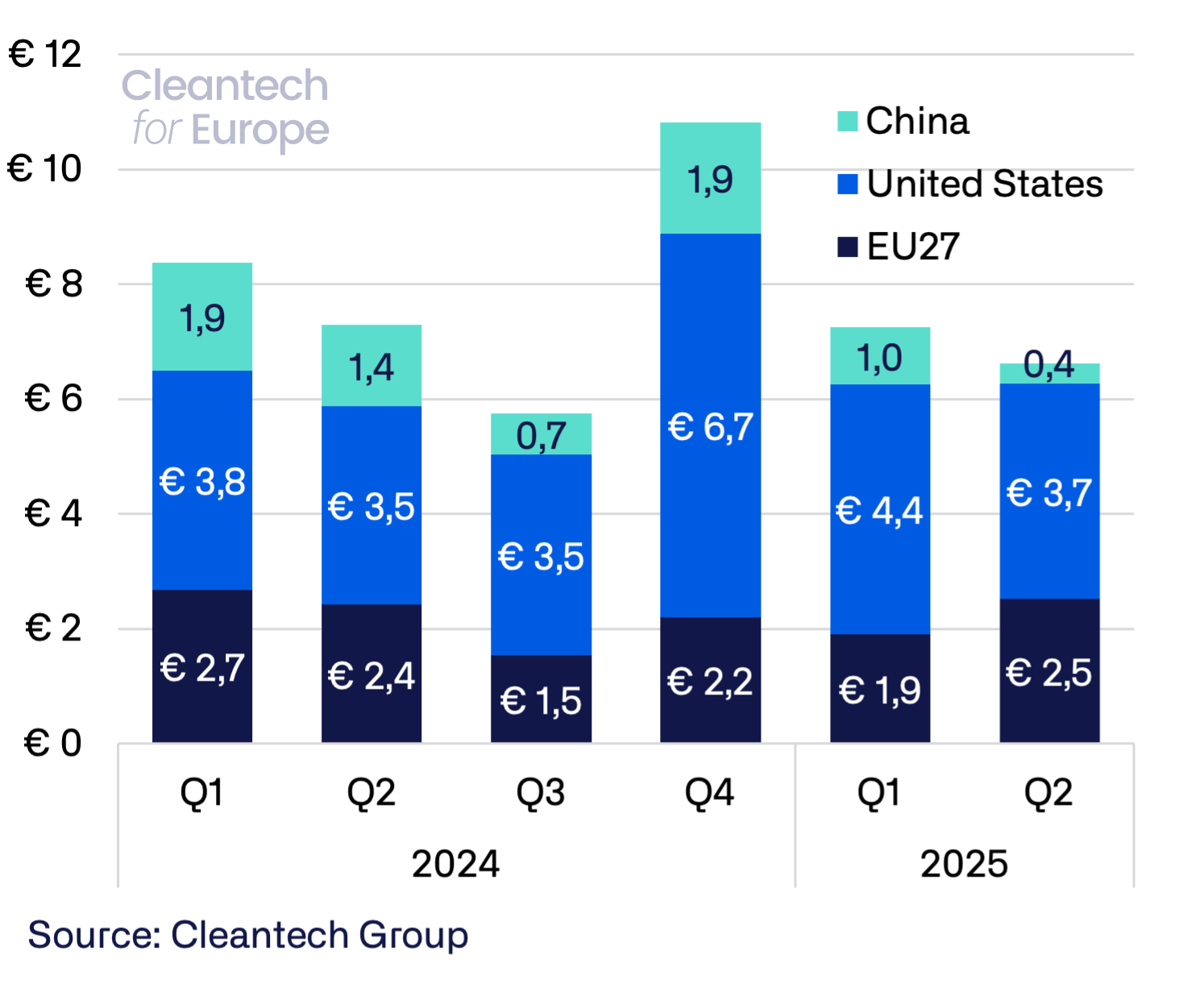

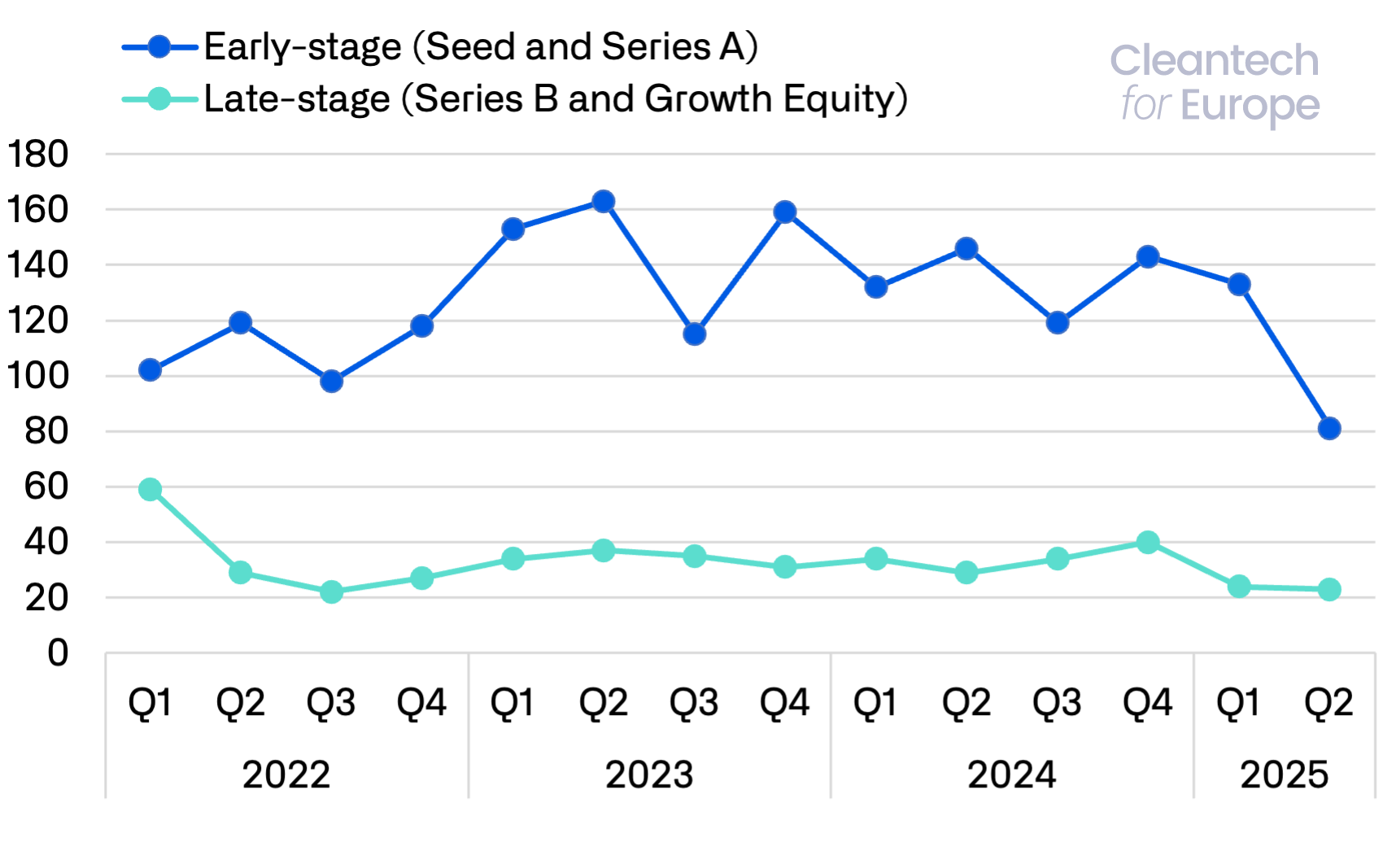

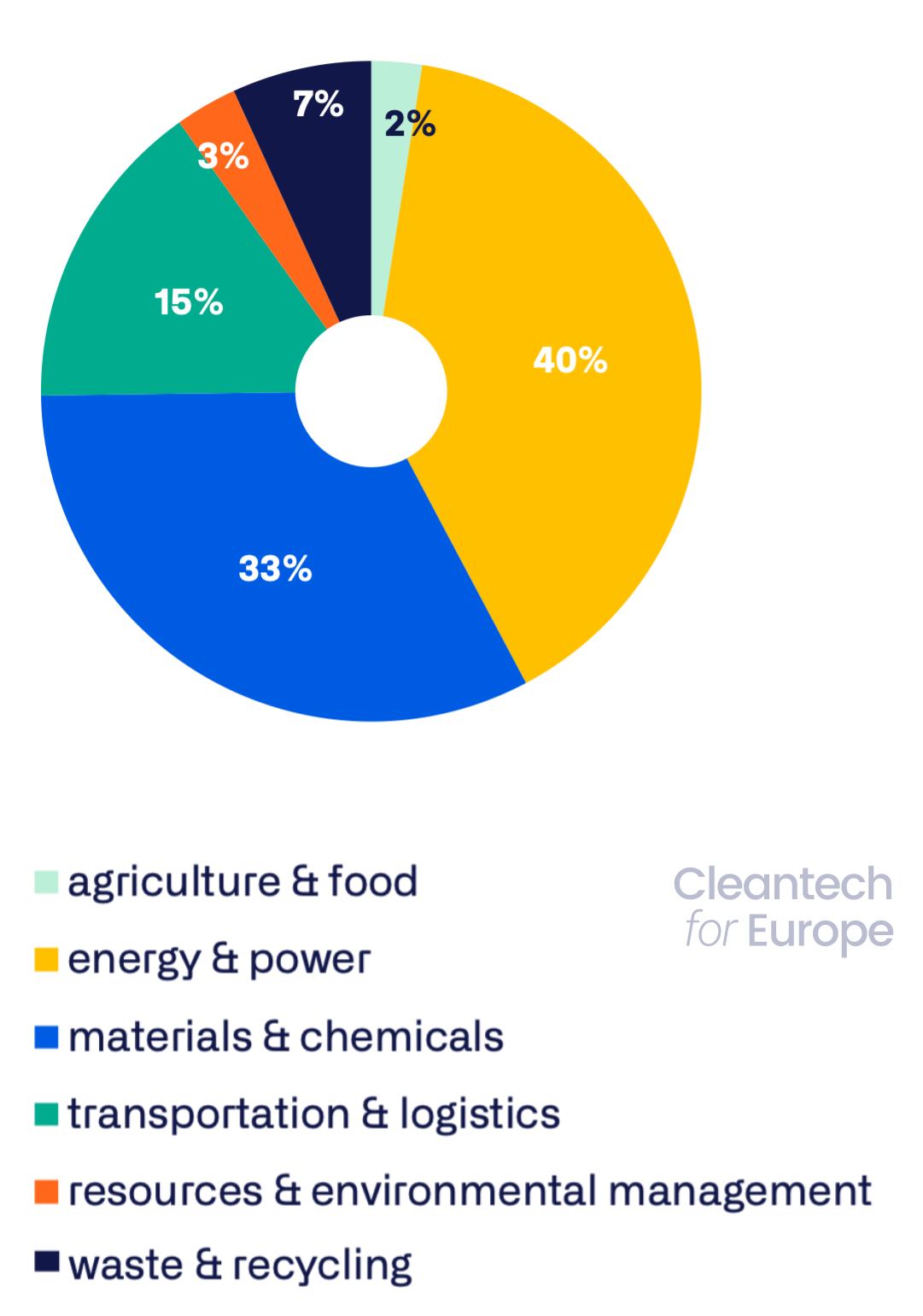

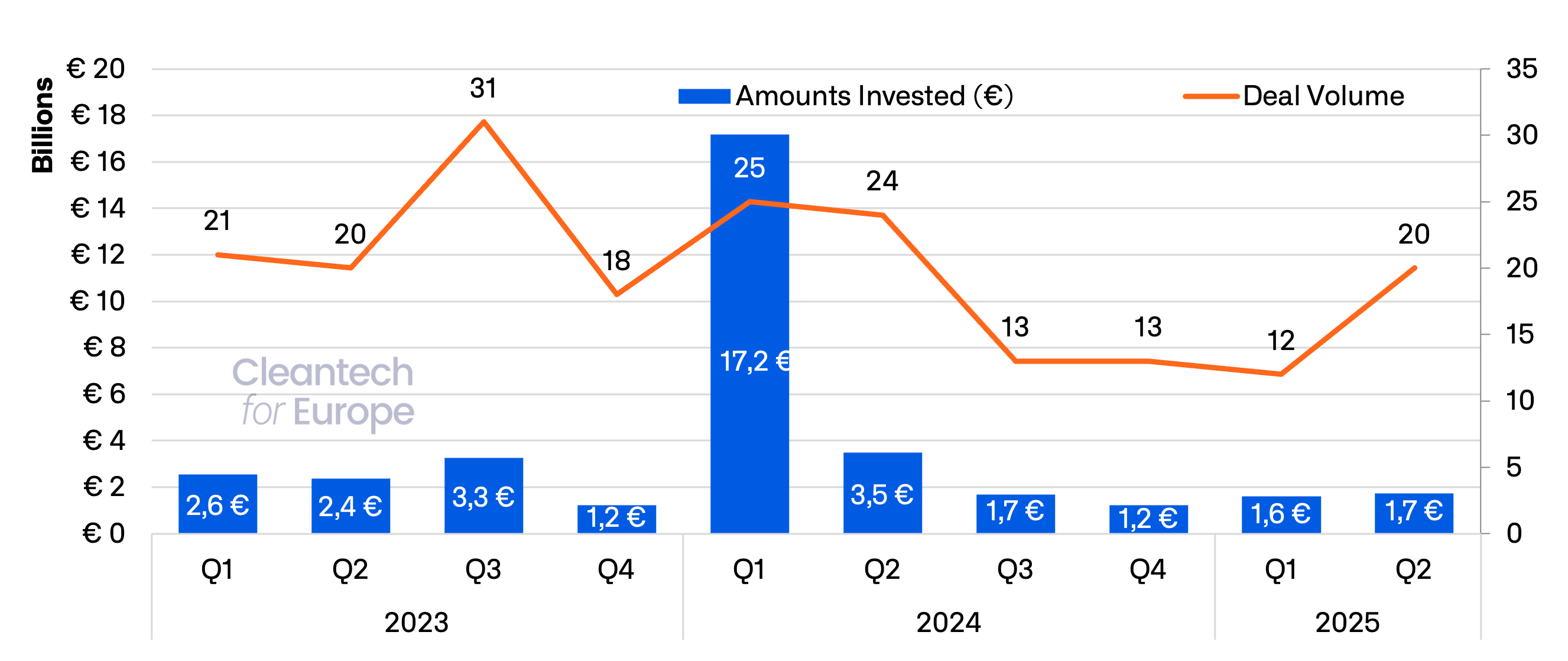

The investment landscape of the cleantech sector in Q2 2025 paints a contrasting picture. EU cleantech venture and growth investment rebounded to €2.5 billion in the last quarter, marking the best quarter in terms of total investment amount since Q1 2024. The average deal size doubled to €24 million compared to Q1 2025, showing bigger deals coming through despite low volumes. The decline in deal volumes reflects a more conservative investment climate, with investors holding off on early-stage ventures and shifting toward safer more liquid investments amidst increased uncertainty and difficulty raising new funds.

This highlights the need for strong demand signals for clean technologies in Europe and for directing public funds in a strategic direction that leverages private capital. The upcoming Industrial Decarbonisation Accelerator Act (IDAA) represents an important opportunity for Europe to create clear and sustained demand signals through lead markets by introducing resilience, sustainability, and ‘Made in Europe’ criteria in public procurement and funding.

Additionally, Europe will have to take decisive action to diversify and control its supplies of Critical Raw Materials (CRMs), as underscored by the security implications of Chinese export bans on CRMs in the context of US-China rivalry. More Clean Trade and Investment Partnerships (CTIPs) and supporting innovation, manufacturing and deployment of critical cleantech that may be less dependent on CRMs will be crucial.

Echoing the need for strong local industries, in July we launched our report

Scale or Fail – A Trade Strategy for Europe’s Clean Industry. While Europe has become a cleantech innovation powerhouse in the last decade, we struggle at scaling these solutions and fostering industrial leadership. Our latest report outlines a bold, practical strategy to boost European competitiveness and security by strengthening local cleantech manufacturing and protecting ourselves from unfair global competition and external dependencies.

Looking back at the last quarter, the Cleantech Friendship Group hosted an event at the European Parliament on how to build Europe’s industrial competitiveness by making the case for local battery cell manufacturing. The European battery industry can deliver on climate targets and create high-quality jobs, and pioneering companies are already building EU industrial capacity despite severe challenges. Moving forward, this promising industry needs to receive production support, demand certainty, and strategic trade measures to unlock its full potential.

Our summer highlight was to welcome our dear friend and cleantech veteran Jigar Shah in Brussels. We had the honour of meeting Commissioner Wopke Hoekstra to discuss opportunities for Europe in the cleantech space and valuable insights from the US Inflation Reduction Act (IRA) and the Loan Programs Office Instruments on how to attract private investors through a strategic allocation of public funds.

This happened in the context of a recently One Big Beautiful Bill Act (OBBBA) passed in the US. The fear of a total rollback of the IRA did not materialise and a more nuanced picture emerged with a repeal of support for wind and solar, but a continued focus on batteries, hydrogen, nuclear, geothermal and CRMs, all against the backdrop of security concerns.

The way forward for Europe is clear: We should not think that the US is abandoning the race for clean industrial leadership. Given also China’s dominance with its state-driven approach, it is pivotal that Europe doubles down and focuses ruthlessly on putting in place a strategic set of policies announced in the Clean Industrial Deal aimed at building industrial leadership in cleantech. Europe has the potential and the capital. What markets need now is a strong sign of optimism from political leaders that we will enact the necessary reforms which are key to more competitiveness and resilience.

.webp)

-min.jpeg)