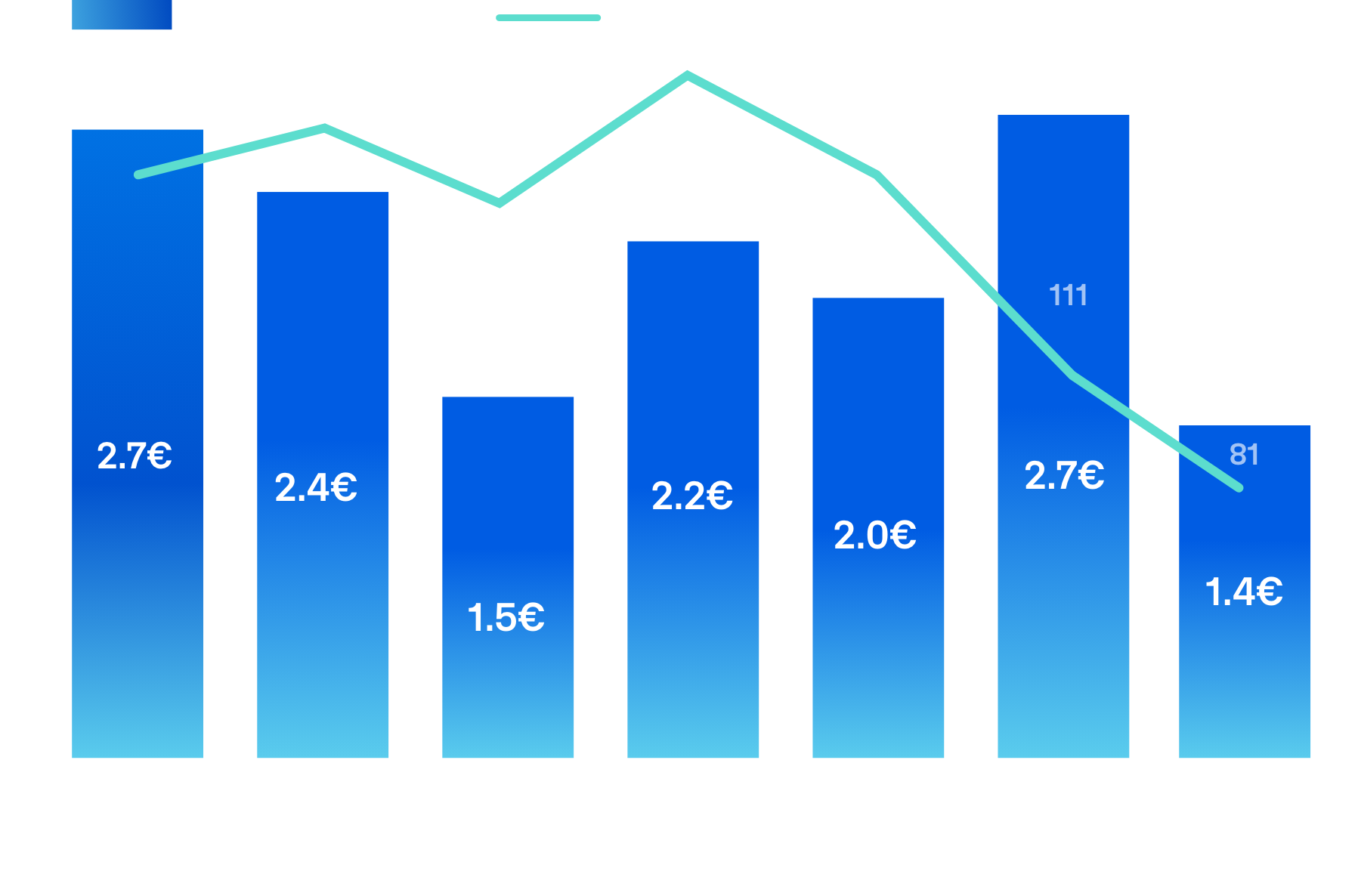

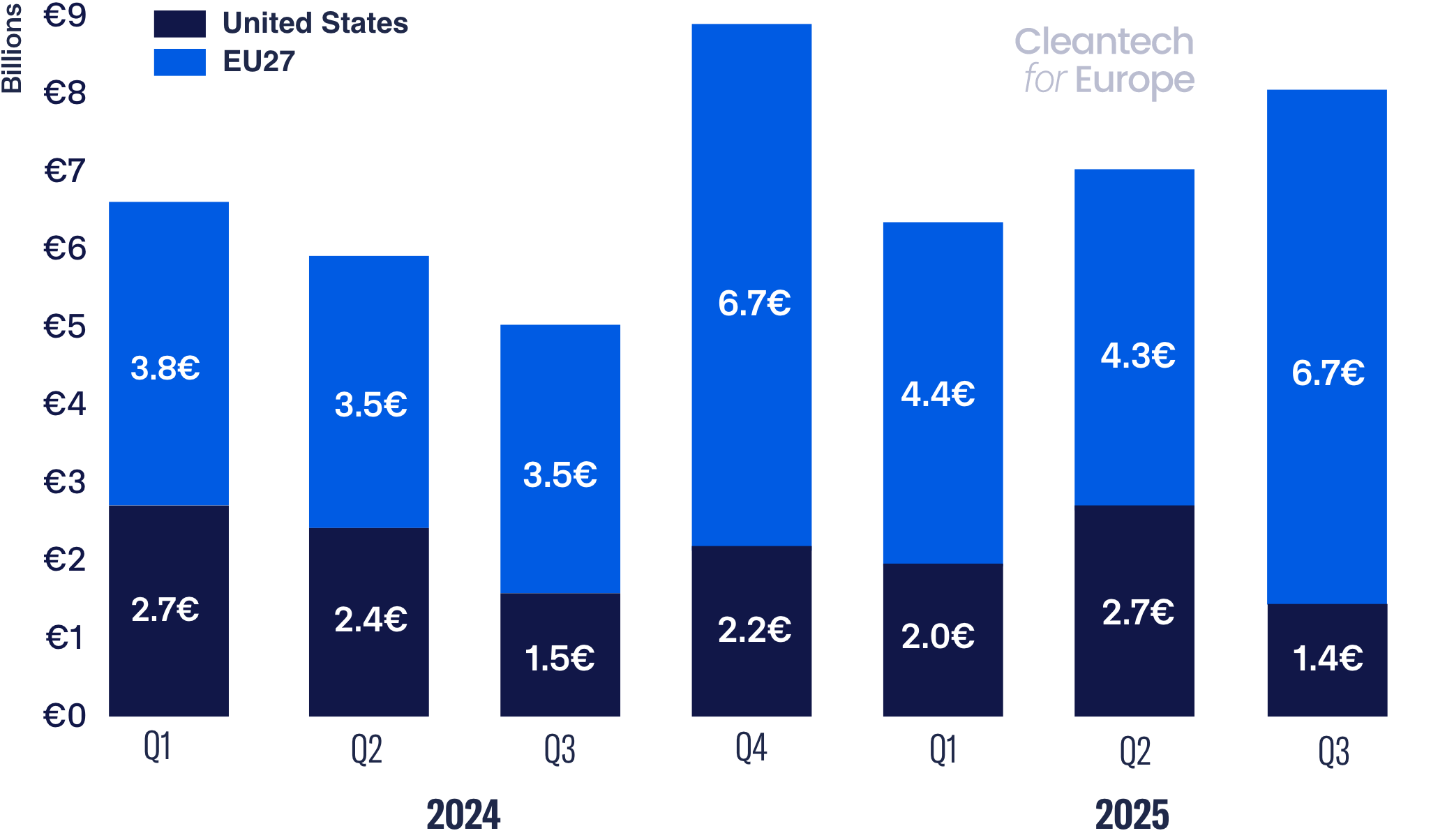

EU cleantech venture and growth investment fell to €1.4 billion in Q3 2025, down from €2.7 billion in Q2 and well below the 2024 quarterly average of €2.2 billion. Total EU deal volume declined to 81 deals, continuing its downward trajectory from 111 in Q2 and 161 in Q1, and marking the lowest quarterly deal count since 2017.

In the US, investment rose to €6.7 billion, its strongest quarter since Q4 2024. However, US deal count fell to just 86, the lowest since at least 2014. The top line figure was driven by a handful of megadeals related to the AI boom, notably in energy-efficient computing and nuclear fusion, reflecting the more concentrated nature of US investment.

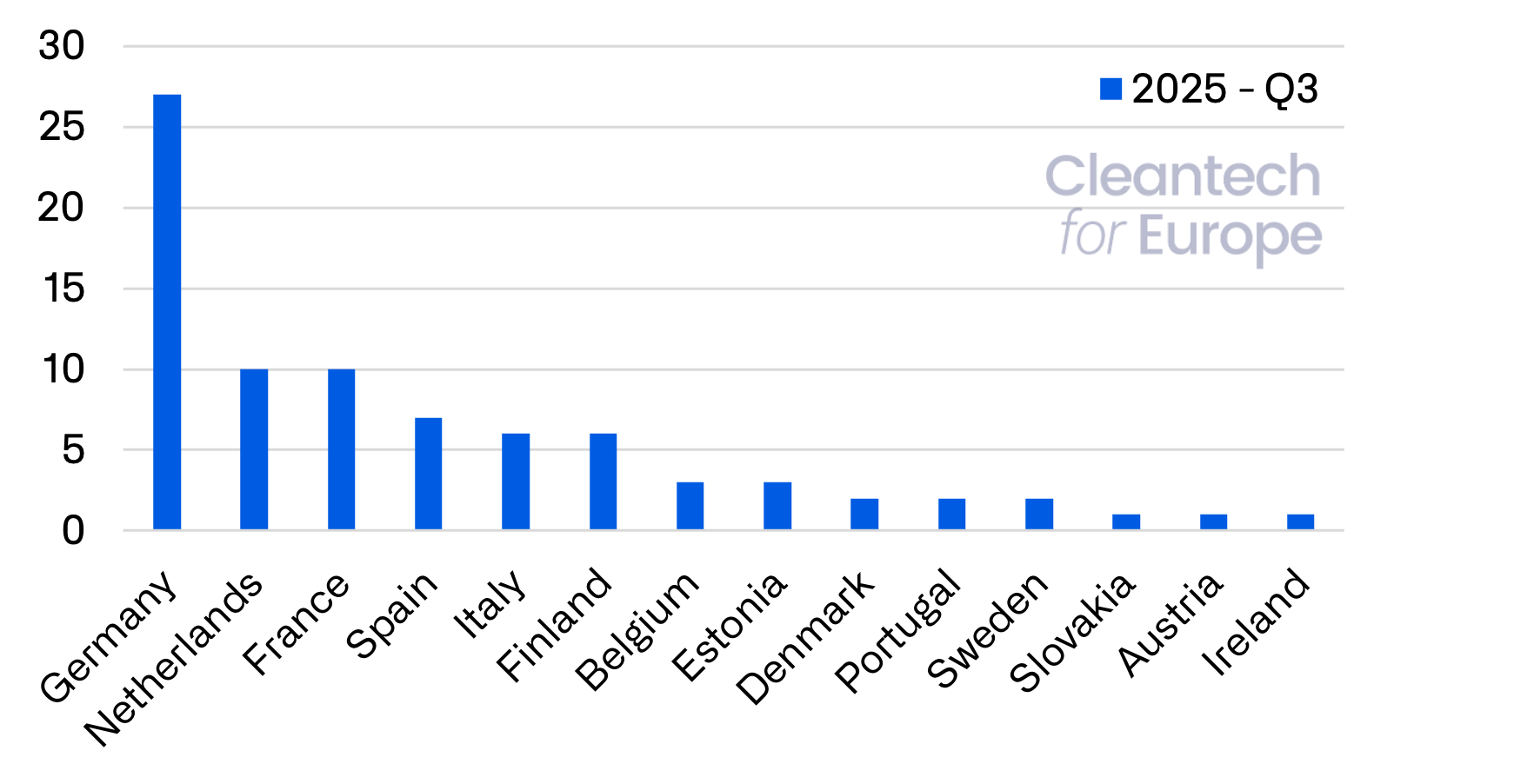

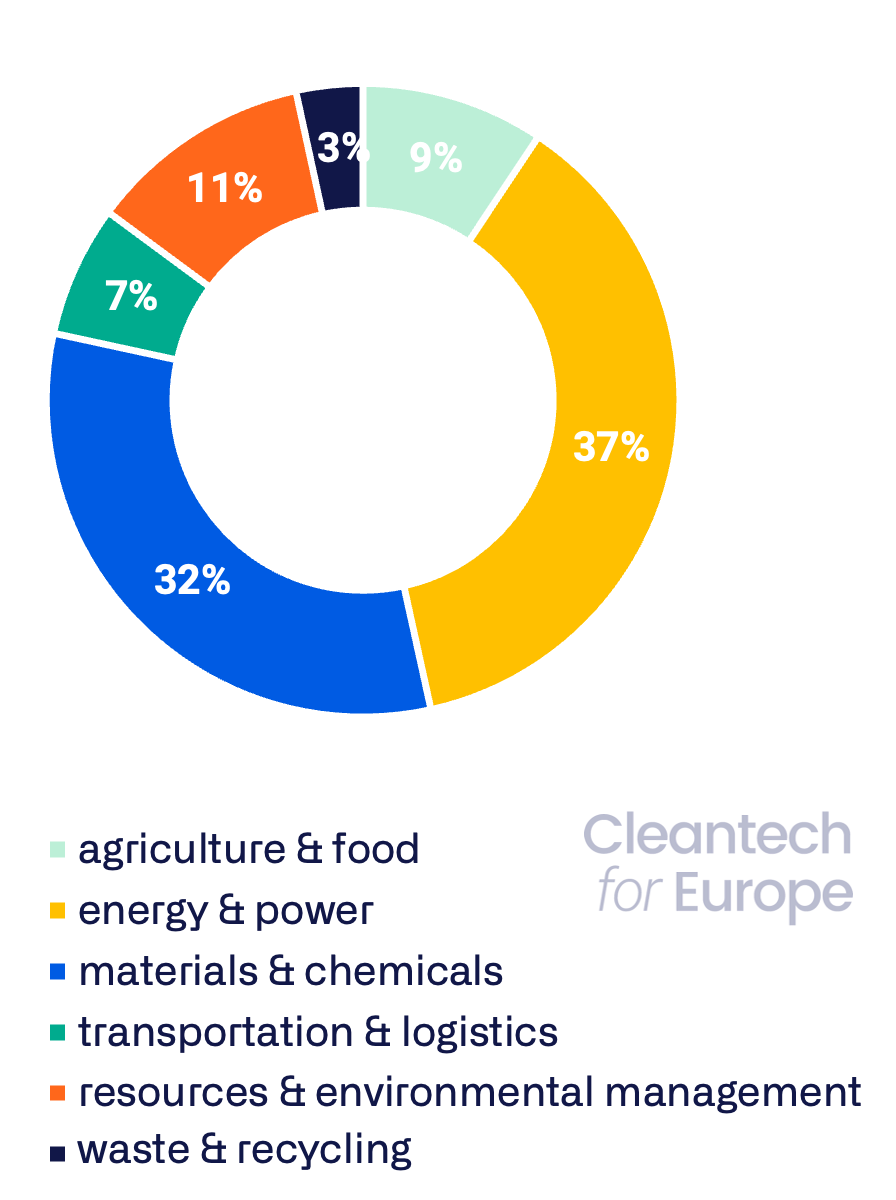

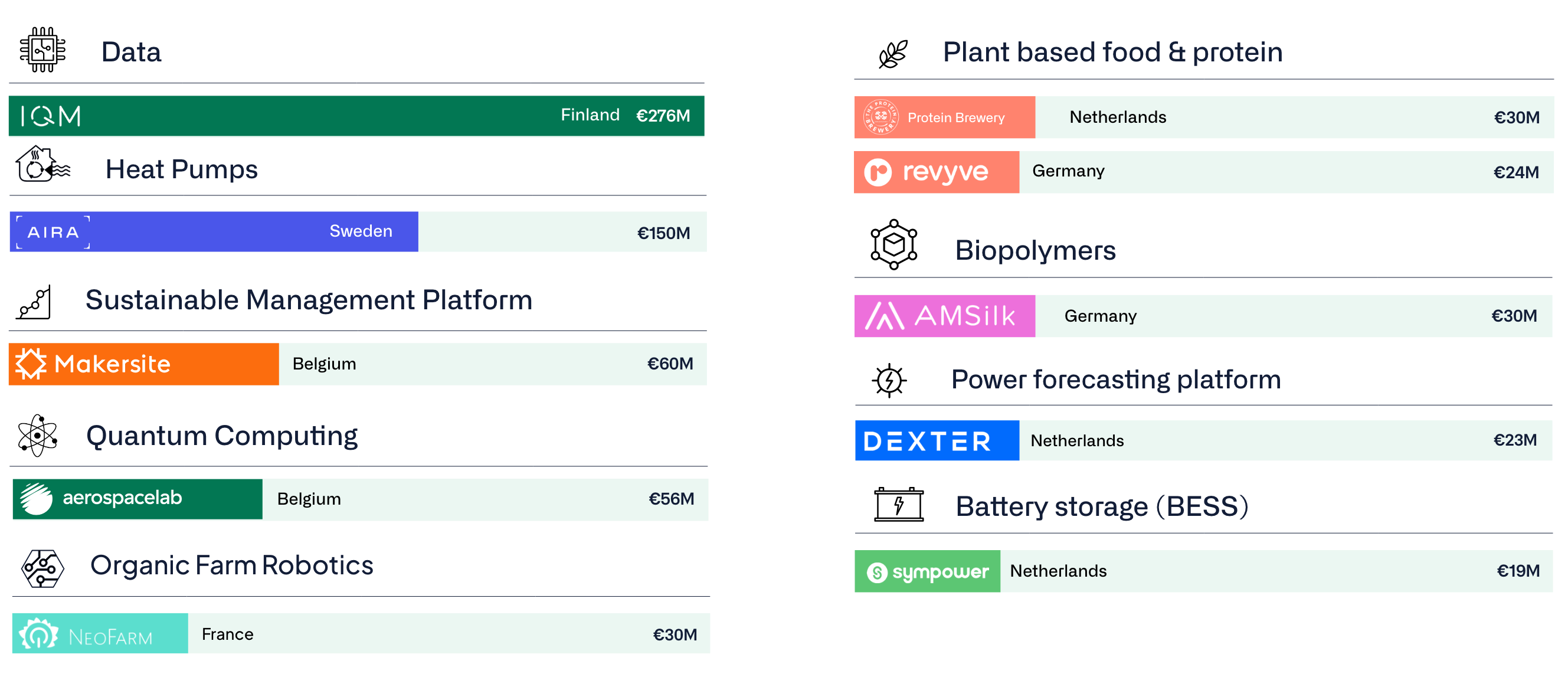

By contrast, EU investment is more distributed across sectors and companies, reflecting Europe’s more advanced clean industrial transformation and steadier regulatory environment, in contrast with US stop-and-go policy dynamics.

Early-stage activity in Europe continued to fall sharply, with 66 deals in Q3 (down from 87 in Q2 and 136 in Q1). Late-stage investment also weakened significantly, with only 15 Series B and growth equity deals, down from 24 in Q2 – the lowest level in more than 5 years. As a result, average deal size fell to €17.4 million, down from €24.6 million in Q2.

Looking ahead, Europe faces macroeconomic uncertainty and rising trade tensions. Clear, long-term policy signals will be essential to restore investor confidence and unlock private capital.

-min.png)

.webp)

-min.jpeg)